On 21 July this year. The Director of National Treasury Information issued an individual interpretation (ref. 0111-KDIB2-1.4010.184.2020.2.AR) concerning the determination of the possibility to take advantage of the exemption

from the obligation to prepare local transfer pricing documentation and the deadline for preparing tax documentation.

The subject of the Applicant’s activity is retail sale of fuel for motor vehicles at petrol stations. In 2019, the Company carried out transactions with capital related entities based in the territory of the Republic of Poland.

The Applicant did not incur any tax loss in the period from 1 January 2019 to 31 December 2019.

The taxpayer was doubtful whether in the case of regulations in force from 1 January 2019 The Company is entitled to take advantage of the premise of exemption from the obligation to prepare local documentation pursuant to Article 11n of the Corporate Income Tax Act with respect to transactions with related domestic entities which have not incurred a loss.

According to the quoted article, the obligation to prepare transfer pricing documentation does not apply to controlled transactions concluded exclusively by affiliates having their residence, registered office or management on the territory of the Republic of Poland in the tax year in which each of these affiliates meets jointly the following conditions:

- does not benefit from the exemption referred to in Article 6,

- does not benefit from the exemption referred to in Article 17(1)(34) and (34a),

- has not suffered a tax loss.

In the opinion of the Applicant, if any of the related companies containing a transaction with the Applicant incurred a tax loss – exemption from art. 11n p. 1 of the Act

The corporate income tax will not apply to a given transaction.

The above position was confirmed by the Director of National Treasury Information.

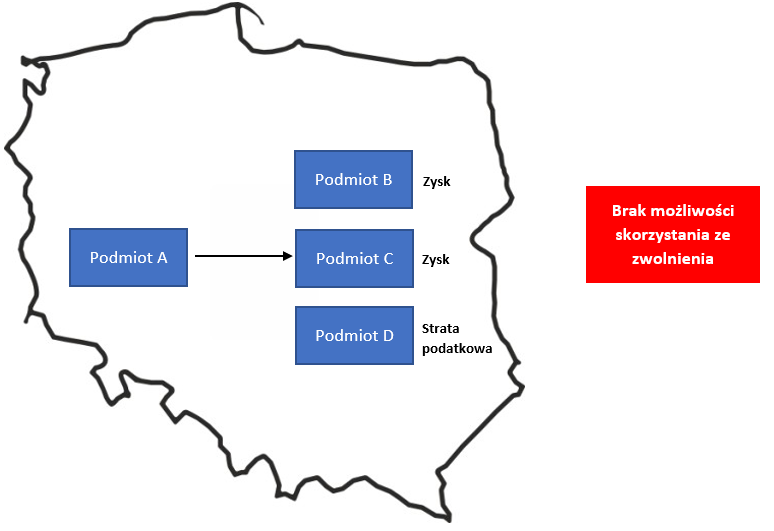

The lack of possibility to take advantage of the described exemption is presented below.

Scheme 1. Exemption from the obligation to prepare transfer pricing documentation pursuant to Article 11n of the Corporate Income Tax Act

For example, entity A sells products to entities B, C and D. All entities are capital related and have their seat in the territory of Poland.

In the light of the position described above, entity A will not be able to take advantage of the exemption from the obligation to prepare transfer pricing documentation due to the fact that entity D suffered a tax loss from the source of revenue under which the above transaction is settled.

Author: Beata Rawa – Transfer Pricing Manager